One of the principal goals of an investment banking process

is to bring buyer choice options to the table for seller clients. A classic

investment process should lead to several high value, qualified buyers meeting

with management. Of course, a premium valuation is key, but often just as

important is the opportunity to select a buyer that has the best culture and

legacy fit.

One other reason to have choices is so that there is a

strong "backup" buyer, or buyers, in place in the event something goes astray

with the initial winning buyer during due diligence, legal and pre-integration.

Unfortunately, this happens more often than clients might expect. While most of

our transactions are consummated with the original buyer, there are several

reasons why a deal could go off the rails. Every one of the examples below has

actually happened in our M&A practice.

Bumped for a bigger, better deal. Buyers have limited

bandwidth and there are times when they might jump ship for a more attractive

deal, leaving our clients out in the cold or on a waiting list. Letters of

Intent are not binding and generally have easy to execute termination clauses.

Problems with financing. Buyers may have some early

indication at the start of the LOI period that they can secure necessary

financing for a deal, but this is usually very preliminary. During due

diligence it is possible that lenders and other financing sources cannot get

comfortable with the transaction.

Discovery of unfavorable core business issues. As

buyers dive deeper into due diligence, it sometimes happens that they learn

things about the business and/or industry that cause them to get cold feet.

This is separate from any misrepresentation type issues. The execution of an

LOI is based on some reasonable level of knowledge but not the kind of complete

knowledge that comes out of a thorough due diligence process.

Re-trading. Unfortunately, there are buyers that will

look to exploit deal momentum and re-trade the valuation, based on spurious

quality of earnings audit claims. Without backup options, sellers may have to

swallow hard and take these valuation hits.

Onerous closing conditions. Aside from valuation

re-trading, buyers may lob in, late-stage, undesirable closing conditions. Some

examples we have seen include: signing then telling staff and clients about the

deal then closing weeks after signing; insisting on customer contract

assignment where they are not legally required; good standing calls with a

large number of customers, beyond the customary three to five such calls.

Accounting and legal disparities. Accounting disputes could range from inventory

valuation to vacation accrual policies. And of course, the ever-fraught working

capital issue, where the buyer is being unreasonable. In a 100-page purchase

agreement, there are more potential legal sticking points than can be brough up

here. While we always lobby our buyers to produce legal documents that are "straight

down the middle", there are buyer lawyers who want to show off and push things

as favorably as possible for their clients.

Delays. Buyers sometimes move slower than planned,

which can lead to seller client frustration and deal fatigue. We have also had

situations where, during an overly long due diligence process, our client's

business performed so well, that is was worth terminating the in place LOI and

going to a backup buyer to re-negotiate a higher valuation.

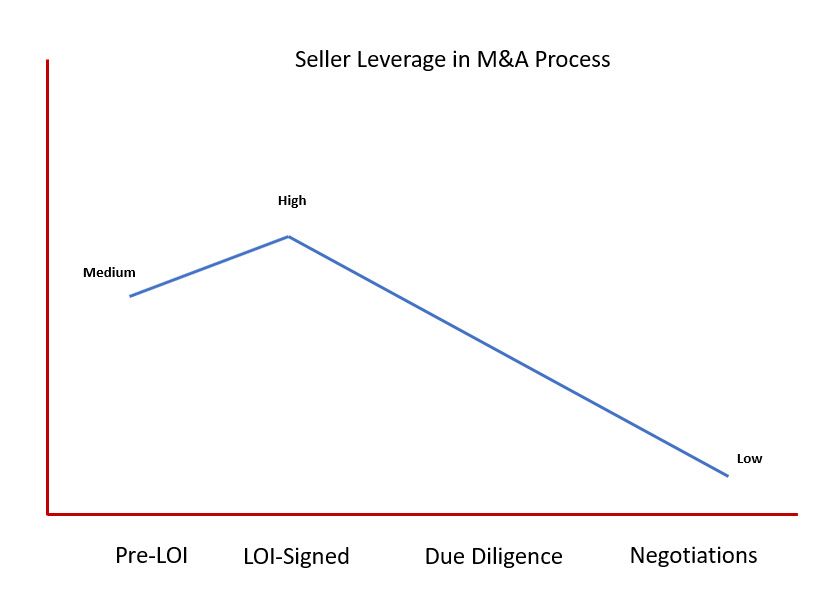

Inherently, seller leverage declines dramatically right

after an LOI is signed with a buyer. The seller is locked into an exclusive,

no-shop period, often 90 days or more. The seller has invested a lot in the

process and is motivated to get a deal done. Buyers can exploit this, even if unintentionally.

Having a strong backup buyer can help shift some leverage to the seller.

We make a point to stay in touch with backup buyers, gauge

their interest and let them know we appreciate their participation in our deal process.

In the cases where we do move to a backup buyer, they are

usually thrilled to have another opportunity for a deal and are eager to be especially

fair. We share with them the issues that scotched the original deal, to coach

them to avoid these if they want to get a deal done with our client.

For sellers who don't use an investment banker and get

sucked into a single suitor negotiation, they don't usually have a backup buyer

option. This is one reason we caution owners not to get stuck in an over the

transom, single suitor buyer situation. In fact, when owners receive a tempting

offer overture, our advice is that this is the perfect time to reach out to a

high quality investment banking firm.

So having a backup buyer is like having a backup generator.

You would prefer to not have to use this, but in case of a problem, it is

always good to have.

Posted by Jeff Wright